Engine Capital, L.P. Sent Letter To The Board Of Directors Of Civeo Corp

Civeo Corporation

333 Clay Street

Suite 4400

Houston, TX 77002

Attention: The Board of Directors (the “Board”)

Members of the Board:

Engine Capital LP (together with its affiliates, “Engine” or “we”) is a large shareholder of Civeo Corporation (NYSE: CVEO) (“Civeo” or the “Company”), with ownership of approximately 9.8% of the Company’s outstanding shares. We invested in Civeo because of the quality of its assets (in particular, its impressive Australian operations), the growth prospects of its asset-light business, its strong financial characteristics, its compelling valuation and our belief that there are readily available opportunities for the Board to significantly increase value for shareholders.

For context, Engine is a value-oriented investment firm launched over a decade ago that manages more than $1 billion in assets on behalf of high-net-worth individuals, endowments and institutional investors. We have a long history of working constructively with boards; since our inception, we have placed more than 44 directors on the boards of 27 public companies. We have followed Civeo for several years and as part of our due diligence, we have had an opportunity to discuss the Company and its prospects with former employees and competitors. We have also had discussions with management, including CEO Bradley Dodson, CFO Collin Gerry and VP of Corporate Development & Investor Relations Regan Nielsen. These discussions have led us to conclude that Civeo has a strong reputation among its customers and is composed of high-quality assets that will continue to generate strong and growing free cash flows in the future.

Despite these attractive characteristics, Civeo has been unable to generate adequate shareholder returns over any relevant period, as shown in the below table.1 Furthermore, the stock trades at a deep discount to its intrinsic value at an EV to 2025 EBITDA multiple of ~3.6x.2

1 Total shareholder returns calculated as of the close on March 14, 2025. Excludes five-year total shareholder return because of COVID-19 impact. Total shareholder returns calculated for the spin-off as of June 2, 2014. Company Proxy Peers include: Badger Infrastructure Solutions Ltd., Black Diamond Group Limited, Dexterra Group Inc., Enerflex Ltd., Forum Energy Technologies, Inc., Matrix Service Company, McGrath RentCorp, Newpark Resources, Inc., Nine Energy Service, Inc., North American Construction Group Ltd., Oil States International, Inc., Precision Drilling Corporation, Select Water Solutions, Inc., Target Hospitality Corp., TETRA Technologies, Inc. and Total Energy Services Inc.

2 Pro forma adjusted for recent Australian acquisition. Assumes pro forma EBITDA of $102 million and net debt at closing of $91 million (end of H1 2025). Assumes Company generates $17.5 million of free cash flow in H1 2025 and pays a dividend on March 17, 2025 (~$3.4 million).

To be fair, this undervaluation and poor performance have not been for a lack of effort from the team. While we believe there have been operational missteps, we acknowledge that over the last few years, Civeo has paid down a significant amount of debt, repurchased a meaningful number of shares, initiated a large dividend and recently announced a deal that makes strategic sense at an attractive valuation. Despite this, the market continues to value Civeo as if it were a dying business at a meaningful discount to its strategic value.

We believe it is time for the Board to take more drastic action to close this large value gap by effectively privatizing the Company, either in the public market through large and aggressive share repurchases to meaningfully shrink the Company’s share count or through a sale of the Company. In parallel, we believe the Company needs to continue to reduce its cost structure. Below is a step-by-step list of initiatives that we believe the Board should immediately launch to unlock value for shareholders:

1. Announce a change in Civeo’s capital allocation model: eliminate the dividend, target a leverage ratio of 1.75x and initiate a large tender offer to repurchase around 25% of the Company’s outstanding shares. This tender should be announced in conjunction with Q1 earnings.

2. Following the closing of the tender offer, enter into an automatic repurchase program and commit to continue repurchasing shares with free cash flows while maintaining a 1.75x leverage ratio.3 Abandon M&A.

3. In parallel with step 2, further reduce the Company’s cost structure.

4. At the right time, initiate a review of strategic alternatives.

Step 1: Announce a Change in Civeo’s Capital Allocation Model

Civeo’s current capital allocation is suboptimal. Given the Company’s deep undervaluation, it is clear that shareholders are not appreciating the current dividend. Therefore, we believe the Board should be opportunistic, completely eliminate the dividend and take advantage of the Company’s depressed share price through a large and immediate repurchase program. When Civeo closes on its Australian acquisition, its leverage will be around 0.9x, leaving it with significant flexibility to further use its balance sheet to create value.4 We note that Civeo’s existing credit agreement allows the Company to increase leverage up to 3.0x. Increasing leverage to a conservative 1.75x would allow Civeo to free up ~$87.5 million that it should immediately use to repurchase around 25% of its outstanding shares.

3 Repurchases subject to continuous undervaluation of the shares.

4 Closing assumed to take place at the end of H1 2025.

To successfully repurchase this many shares and given the illiquidity of the stock, the Board will have to pay a premium. Practically, this should be done through a Dutch tender offer, which will end up being cheaper than trying to effectuate these repurchases in the open market. We therefore recommend that in conjunction with the announcement of Q1 earnings, Civeo announces a Dutch tender offer to repurchase shares between $24 and $28 per share.5 If the tender takes place at the midpoint of this range, the Company will repurchase 3.4 million shares or around 25% of the Company’s outstanding shares. This range is illustrative. Given Civeo’s undervaluation, it is very possible that to repurchase ~$87.5 million of shares, the Company will have to pay a higher price, which would still be worth it given the value creation opportunity under our new capital allocation policy.

If for some unforeseen reason, the Australian acquisition is not completed, Civeo’s leverage post tender would be 1.3x, an even more conservative ratio than if the acquisition closed, in which case the leverage would be 1.75x.

Step 2: Enter Into an Automatic Repurchase Program and Commit to Repurchasing Shares With Free Cash Flows While Maintaining a 1.75x Leverage Ratio; Abandon M&A

As the recent announcement of the Australian acquisition has highlighted, M&A is not the answer for Civeo. Acquiring assets similar to the core business is not going to change the market’s perception of the Company or rerate its stock – instead, it introduces unnecessary operational and financial risks for shareholders. The failed acquisition of Noralta Lodge in 2018 under the current leadership is an example of those risks. Shareholders would be better off having the Company maintain its 1.75x leverage and commit to using all its free cash flows to repurchase shares until they are fairly valued. A commitment from the Board is particularly important because it would remove any ambiguity regarding capital allocation. Shareholders wouldn’t worry about poor M&A, for example. Because of this clarity, we believe such a commitment is likely to reduce the Company’s cost of capital and help rerate Civeo’s trading multiple.

We estimate that Civeo will generate around $89.5 million of free cash flow (after the incremental interest from increasing the leverage ratio to 1.75x) from H2 2025 through 2027.6 This represents ~32% of the Company’s current market capitalization (this statistic alone is striking and underscores how undervalued Civeo is). If the Board uses this capital to repurchase shares at an average price of $30 per share, it can repurchase another 3 million shares, or around 22% of the Company’s current share count. If the Company is unable to buy this number of shares in the market, it may end up having to do additional tenders.

The Board may be concerned about reducing the liquidity of the stock through these aggressive repurchases. We believe this fear would be misplaced. The stock is already very illiquid and making it more illiquid is unlikely to concern shareholders. In any event, it is possible that committing to an unambiguous capital allocation policy helps rerate the stock and improve its liquidity. If the Board can buy the business it knows best at a material discount to its intrinsic value, it should do so consistently since it will be tremendously accretive to the remaining shareholders.

5 For modeling purposes, we have assumed that the tender and the acquisition close at the end of H1 2025.

6 Assumes Civeo generates ~$43 million of free cash flow annually from 2025 through 2027 proforma of the Australian acquisition (before increasing leverage to 1.75x) less incremental interest expense of ~$7 million per year (starting in H2 2025) due to increased leverage. 2025 free cash flow assumes the recently announced acquisition closes at the end of H1 2025.

Step 3: In Parallel With Step 2, Further Reduce the Company’s Cost Structure

While leadership has begun rightsizing the Company’s cost structure, we believe management and the Board need to go further to offset the significant decline experienced in Civeo’s Canadian business. In particular, corporate overhead in Houston at close to $30 million per year is a significant drag to the Company’s returns.

As we look at the Company’s cost structure, the following questions come to mind:

· Given the decline in the Canadian operations, can the Company justify having a separate headquarters in Houston, where there are no operations?

· Can the Houston headquarters be folded into the Canadian or Australian operations?

· How much could be saved if the Houston positions were folded into one of the two geographies?

· Does Civeo need to trade on the NYSE? Would it be cheaper to trade on the TSX or the ASX? Would this also lead to a reduction in audit or other compliance fees?

· Given the Company’s size, valuation and long-term TSR, can Civeo afford to pay its CEO $6 million per year? 7

· Does Civeo need a nine-person Board for a total cost of almost $2 million? 8

· Are there additional opportunities at the divisions where overhead remains elevated despite the recent restructurings?

From our discussions with numerous former employees, it is clear that there are opportunities to meaningfully reduce costs. We would advise the Board to get outside help to receive unbiased answers to the questions we raised above.

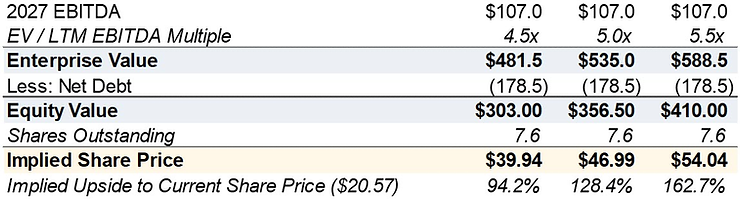

If the Board follows our capital allocation recommendations, we believe that by the end of 2027, the stock could conservatively be worth between $40 and $54 per share, an upside of nearly 130% at the midpoint of this valuation range: 9

7 The CEO’s compensation was $6.3 million, $4.7 million and $5.1 million in 2023, 2022 and 2021, respectively.

8 Total Board compensation was $1.97 million in 2023.

9 Illustratively assumes EBITDA remains flat at $102 million through 2027. Assumes an incremental $5 million of cost savings. Assumes share-based compensation dilution from 2025 through 2027 in line with prior years and assumes all free cash flow is used for repurchases starting in H2 2025 after the tender offer is completed.

Step 4: At the Right Time, Initiate a Review of Strategic Alternatives

It is obvious that Civeo is not a good U.S. public company, and that the Company’s discounted valuation is largely a result of structural problems. While Civeo is listed in the U.S., it operates in Canada and Australia, jurisdictions that are less familiar to most U.S. analysts. The Company is also subject to currency risks, which create additional obstacles for American investors, and its business is tied to legacy industries such as oil and coal, which create additional restrictions for ESG-concerned investors. Civeo has no pure play U.S. public peer of a similar size or geographic composition, making it difficult for public market investors to evaluate and diligence it. Finally, the Company is subscale with a large overhead structure.

Given these dynamics, we believe Civeo is unlikely to reach its intrinsic value in the public market and a sale is likely to deliver returns superior to the standalone path. Regardless of whether Civeo’s various assets are sold together or transacted separately, a combination with one or multiple strategic acquirers will create significant synergies. At a minimum, most of the $30 million in corporate overhead could be eliminated and additional overhead costs in Canada or Australia could also be targeted, depending on the buyer.

The below table calculates the strategic value of Civeo if a sale were to take place at the end of 2025, following the tender and additional share repurchases in 2025. We have modeled the repurchase of 3.4 million shares in the tender followed by another 0.6 million of shares repurchased in H2 2025 ($18 million generated in H2 2025 divided by $28 per share as an illustrative price), resulting in a share count of 9.8 million at the end of 2025.10

Based on comparable transaction multiples, we believe Civeo could be sold at a price between $39 and $50 per share, representing a nearly 116% premium to the current trading price at the midpoint of the range. Assuming the strategic acquirer can cut $30 million in overhead, this price would represent a fully synergized multiple of 4.6x EBITDA.

In our discussions with public companies, we often find that management teams and boards are reluctant to start a sale process unless they have already been approached by a potential buyer. We believe this reasoning is flawed and that the Board should not view a potential lack of interest as indicative. Instead, the Board should proactively approach buyers who can then diligence the Company appropriately. We believe such a process is likely to yield a very satisfactory outcome for all parties involved.

10 H2 2025 free cash flow includes incremental interest expense from increased leverage. Assumes share-based compensation dilution in 2025.

In conclusion, we believe the status quo is no longer tenable. Management and the Board need to take a more proactive stance to unlock value for investors. We request a meeting with members of the Board at your earliest convenience to discuss the matters and initiatives we have set forth in this letter. On behalf of Engine, we look forward to working with you to increase long-term shareholder value.

Sincerely,

/s/ Arnaud Ajdler

Arnaud Ajdler

Managing Partner

Source:

https://www.sec.gov/Archives/edgar/data/1580320/000092189525000839/ex991to13da209488cveo_032025.htm

Member discussion